You generally think of tax loss harvesting as a year-end strategy. And it truly is a good one.

But it’s also a “whenever you need it” strategy.

For example, say you used a lot of “kick the can down the road” strategies this year and need a big loss to offset gains in 2024. You can set up that accomplishment now.

When you make what turns out to be an ill-fated investment in a taxable brokerage firm account, the good news is that you can harvest a tax-saving capital loss by selling the loser security. Right? Well, maybe not.

You could destroy that loss deduction by running afoul of the dreaded wash sale rule.

Let’s say you have harvesting tax losses to offset gains on your mind.

Here’s the current story on

- How the Wash Sale Rule Works

- how the wash sale rule works,

- a couple of ways to defeat it,

- some questionable IRS positions on the subject, and whether the rule applies to cryptocurrency losses.

How the Wash Sale Rule Works

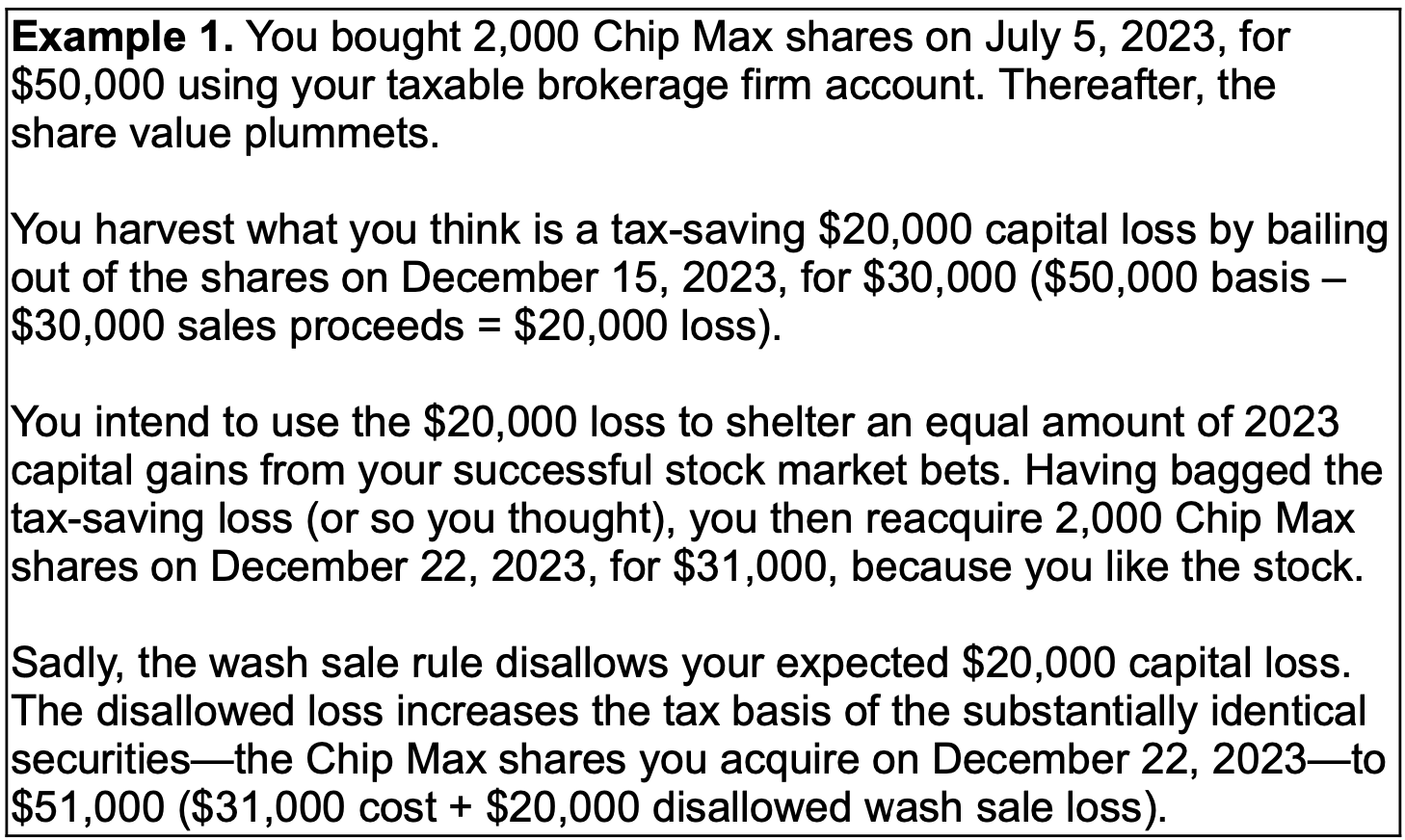

For federal income tax purposes, a loss from selling stock or mutual fund shares is disallowed if, within the 61-day period beginning 30 days before the date of the loss sale and ending 30 days after that date, you buy substantially identical securities.

The theory behind the wash sale rule is that the loss from selling a security and acquiring substantially identical securities within the 61-day window adds up to an economic “wash.” Therefore, you’re not entitled to claim a tax loss.

Fortunately, when you have a disallowed wash sale loss, the loss doesn’t vaporize.

Instead, the general rule is that the disallowed loss is added to the tax basis of the substantially identical securities that triggered the wash sale rule. When you eventually sell substantially identical securities, the additional basis reduces your tax gain or increases your tax loss.

Two Ways to Defeat the Wash Sale Rule

Defeating the wash sale rule is only an issue when you want to sell a security to harvest a tax-saving capital loss but still want to own the security because you expect it to appreciate above the current price.

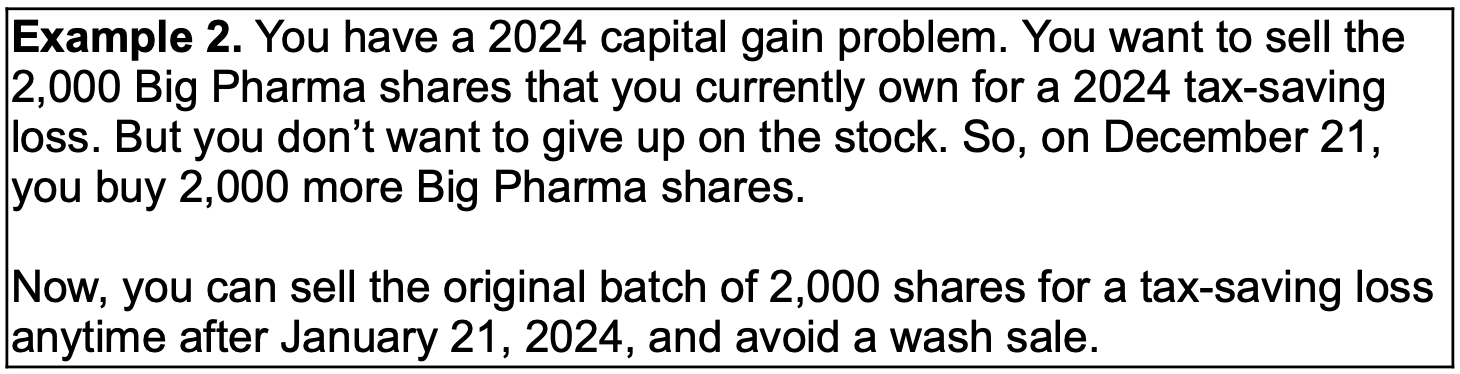

One way to defeat the wash sale rule is with the “double up” strategy: You buy the same number of shares in the stock you want to sell for a loss. Then, you wait 31 days to sell the original batch of shares. When all is said and done, you’ve made a tax-saving loss sale, but you still own the same number of shares as before and can, therefore, still benefit from the anticipated appreciation.

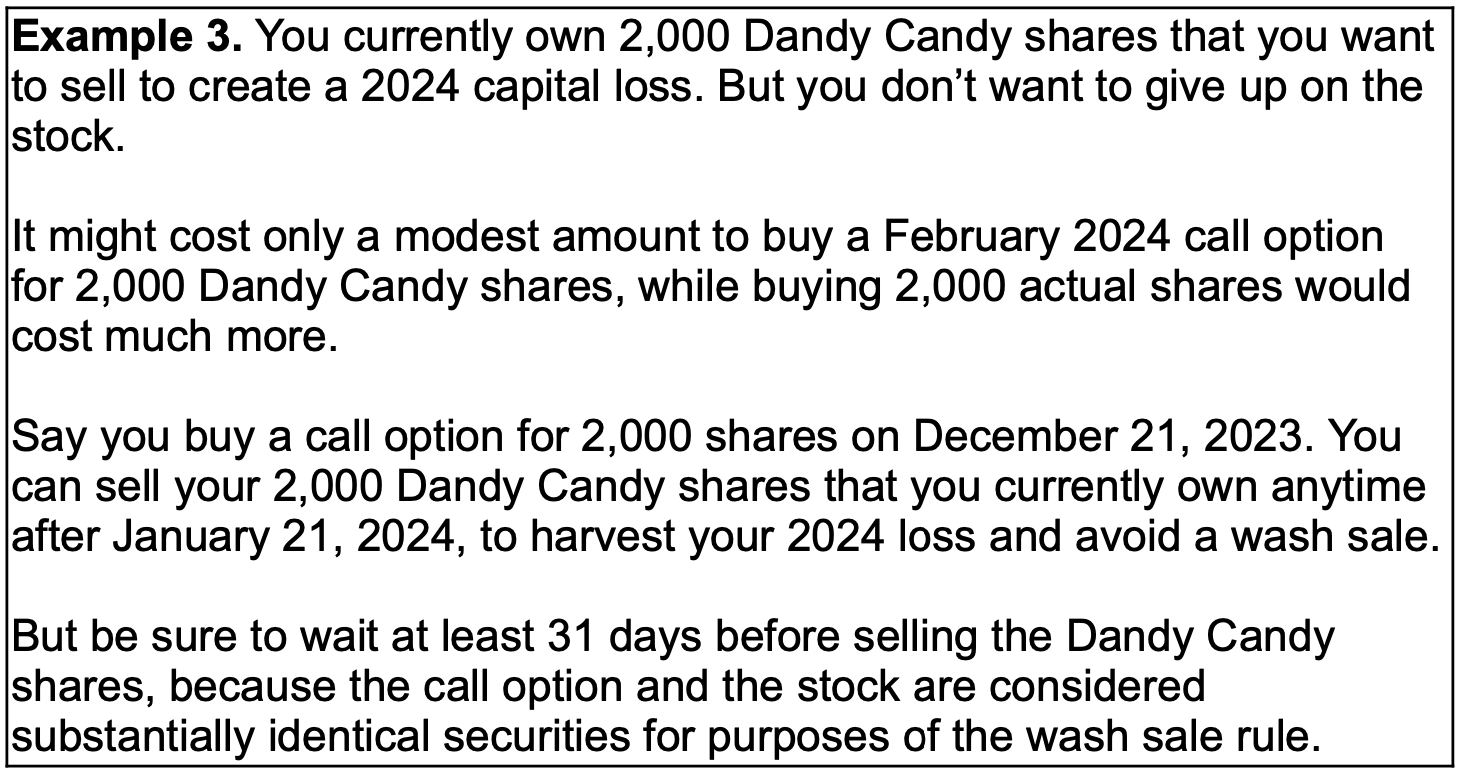

Example 3 (below) may be a much less expensive way to achieve essentially the same tax-saving goal. Try to buy a relatively inexpensive call option on the stock you want to sell for the 2024 tax loss. Then, wait more than 30 days to sell the stock.

Does the Wash Sale Rule Apply When a Related Party —Including Your IRA—Acquires Substantially Identical Securities?

Good question. If you sell stock for a loss and your spouse buys identical stock within the forbidden 61-day period, it does not seem unreasonable to believe that the wash sale rule applies if you file jointly with your spouse— because you and your spouse are treated as one taxpayer.

But nothing in our beloved Internal Revenue Code or IRS regulations addresses this situation. IRS Publication 550 simply says that the wash sale rule applies if your spouse acquires substantial identical securities within the 61-day period—without mentioning the situation where you and your spouse file separate returns. Once again, this situation is not addressed in the Internal Revenue Code or IRS regulations.

According to Publication 550, the wash sale rule also applies when your controlled corporation acquires substantially identical securities within the forbidden 61-day period. The support for this anti-taxpayer notion is apparently a 1935 court decision that was decided long before the current wash sale rule existed.

Finally, what happens if you use your tax-favored retirement account—IRA, 401(k), etc.—to buy substantially identical securities?

According to IRS Revenue Ruling 2008-5, having your traditional or Roth IRA buy substantially identical securities within the forbidden 61-day period triggers the wash sale rule. Even worse, Revenue Ruling 2008-5 says that you cannot increase the basis of your IRA by the amount of the disallowed loss. Therefore, according to the IRS, the disallowed loss simply goes up in smoke.

These anti-taxpayer epiphanies rely on a 1933 court decision where substantially identical securities were acquired by a taxable trust that was controlled by the taxpayer.

Revenue Ruling 2008-5 notes that an IRA is a tax-exempt trust, whereas the trust in the 1933 Security First National Bank case was a taxable trust, and then ignores the distinction. It seems fair to observe that the distinction between a taxable trust and a tax-exempt IRA trust is a pretty big one that should not be so carelessly dismissed.

Bottom line. IRS regulations dealing with the wash sale rule have been on the books since 1956, but they don’t address any of the aforementioned “related party” circumstances. Therefore, we think you can take the self-serving IRS positions above for what they are worth.

That said, consult with your tax pro if the issue of whether the wash sale issue applies comes up in any of the above-mentioned situations.

Cryptocurrency Losses Are Exempt from the Wash Sale Rule (for Now)

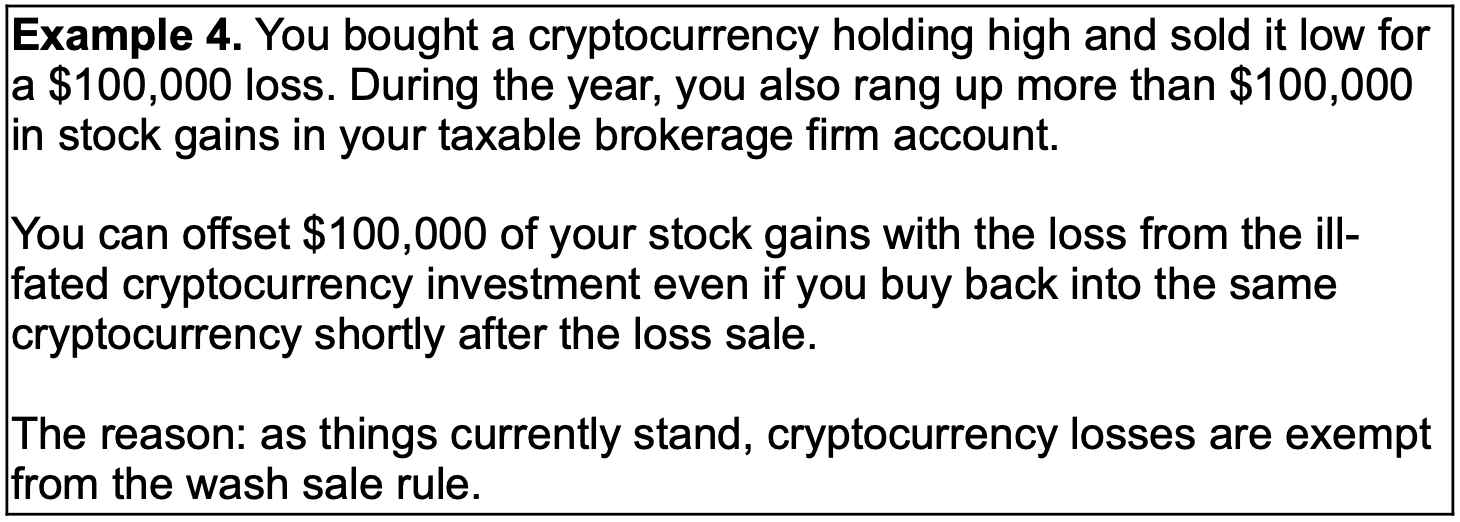

The IRS currently classifies cryptocurrencies as “property” rather than securities. That means the wash sale rule does not apply if you sell a cryptocurrency holding for a loss and acquire the same cryptocurrency shortly before or after the loss sale.

In this case, you just have a garden-variety short-term or long-term capital loss, depending on your holding period. No wash sale rule worries.

This favorable federal income tax treatment is consistent with the long-standing treatment of foreign currency losses.

It would probably take an act of Congress to make cryptocurrency losses subject to the wash sale rule, but that could happen. Stay tuned for possible developments.

Warning. Losses from selling crypto-related securities, such as Coinbase stock (Nasdaq: COIN), fall under the wash sale rule because the rule applies to losses from assets classified as securities for federal income tax purposes. Stocks such as Coinbase are securities, while cryptocurrencies themselves are not currently classified as securities.

Takeaways

Harvesting capital losses is a tried-and-true tax planning strategy. And it’s a strategy you can use anytime the opportunity is there, and you need to harvest a loss.

But always make sure you defeat the wash sale rule.

In this article, you

- saw how the wash sale rule works,

- learned a couple of ways to defeat it,

- noted some questionable IRS positions on the subject and

- learned that the wash sale rule does not apply to cryptocurrency losses.

In conclusion, tax loss harvesting is a valuable and versatile strategy for optimizing your tax situation, effective at year-end and whenever necessary. This article has illuminated the intricacies of the wash sale rule, a key consideration in this process. You’ve discovered how this rule functions, methods to legally circumvent it, and the IRS’s stance on related issues, including its applicability to cryptocurrency losses. Remember, while cryptocurrencies currently escape the wash sale rule, this could change with future legislation. As always, it’s crucial to stay informed and consult with a tax professional to navigate these complexities effectively and ensure that your tax loss harvesting strategy remains both compliant and beneficial.

{kind=link}