If you sell goods and services and are paid through a third-party settlement organization (TPSO), such as PayPal, the IRS changed the likelihood of your receiving a 1099-K.

Here’s what you need to know about IRS Form 1099-K.

What Is Form 1099-K?

IRS Form 1099-K, Payment Card and Third Party Network Transactions, is used to report to the IRS payments for sales of goods and services where payment is made (a) with a payment card or (b) through a TPSO.

The payment card company or TPSO sends the required 1099-Ks to the recipient, the IRS, and the recipient’s state tax department. The deadlines for filing are

- January 31 for payees (those who received the money) and

- February 28 for the IRS copy, or March 31 if filed electronically.

The rules for when Form 1099-K must be filed differ depending on whether payment is by payment card or through a TPSO.

Payments by Payment Card

Payment cards include credit cards, debit cards, and stored-value cards (including gift cards).

If you sell goods or services and your customers or clients pay you directly by credit, debit, or gift card, you’ll get a Form 1099-K from the payment card company or payment settlement entity, no matter how many payments you got or how much they were for.

In other words, there is no dollar threshold that triggers the filing of Form 1099-K for payment card payments.

The IRS made no changes to this rule. It continues in place for payments made in 2023.

Payments through TPSOs

Third-party settlement organizations function as intermediaries between buyers and sellers of goods or services and charge a fee for doing so. They include

- payment apps such as PayPal, Cash App, and Venmo;

- online auction or marketplace services such as eBay and Amazon;

- gig economy platforms such as Uber and Airbnb;

- some cryptocurrency processors such as BitPay;

- craft or maker marketplaces such as Etsy;

- ticket exchange or resale sites such as Ticketmaster and

- some crowdfunding platforms.

When Form 1099-K came into use in 2011, TPSOs were required to report payments for goods and services they processed for customers only if the recipient had

- gross annual earnings over $20,000 and

- more than 200 transactions in the calendar year.

With these thresholds, only relatively frequent users of TPSOs exceeded both thresholds and had their payment information reported to the IRS.

Loophole

These rules left a big reporting hole for businesses that are paid through TPSOs. Unlike when they are paid by cash or check, there is no requirement that a client or customer who pays a business through a TPSO such as PayPal file Form 1099-NEC (formerly Form 1099-MISC) and report the payment to the IRS.

Such 1099 reporting is left to the TPSO by filing a 1099-K.4 So no 1099 of any kind was filed for businesses paid through a TPSO when they were paid less than $20,000 or had fewer than 200 transactions.

As more and more businesses came to be paid through TPSOs, Congress decided the 1099-K reporting loophole should be closed.

The New Law

When Congress enacted the American Rescue Plan Act of 2021, it amended the law to require that TPSOs file Form 1099-K for any payee paid more than $600 during the year, with no minimum transaction requirement—the same rule applicable to the filing of Form 1099-NEC.

The change in the reporting rules was supposed to take effect for the 2022 tax year, but the IRS delayed it until the 2023 tax year. Now, the IRS has decided to delay implementation yet again, as follows:

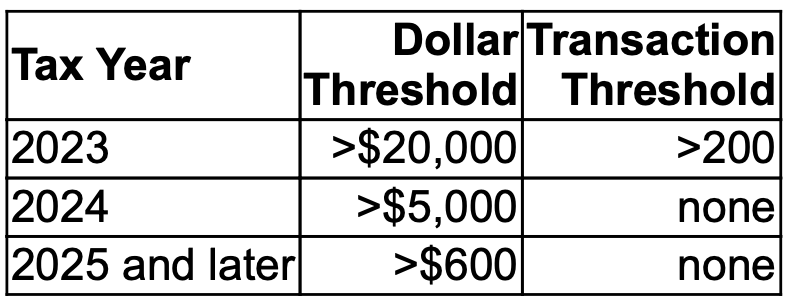

- For the 2023 tax year, the $20,000 and 200 transaction thresholds continue to apply.

- For the 2024 tax year, the $20,000/200-transaction threshold will be eliminated, and a $5,000 threshold will apply with no transaction threshold—in other words, a TPSO must file a 1099-K in 2024 if it pays a payee more than $5,000 in 2024, regardless of the number of transactions.

- For the 2025 tax year and later, the $600 threshold is scheduled to apply again with no transaction threshold.

Here’s a summary:

Thus, for example, if you received $6,000 in total payments from a TPSO such as PayPal in 2023 and had only 100 transactions, PayPal won’t send you a 1099-K.

If you receive $6,000 in 2024, the TPSO will file a 1099-K in 2024, regardless of the number of transactions. The same goes for payments received in 2025 and later.

Can the IRS Do This?

Can the IRS decide on its own to delay the implementation of a tax law enacted by Congress? Apparently so. The IRS claims to have broad discretion to delay the implementation of complex laws in the interest of good tax administration.

There is one exception to the delay in the new reporting rules: TPSOs that perform backup withholding for payees during calendar year 2023 must file a 1099-K if they pay that payee more than $600.9 Backup withholding is required when the payee’s taxpayer identification number is not obtained by the TPSO.

Why All the Delays?

Why all the delays in implementing the new reporting rules?

Because the IRS fears it will be inundated by 44 million new 1099-Ks, many of which will be filed by mistake by TPSOs and confuse taxpayers.

Personal payments from family and friends should not be reported on Form 1099-K because they are not payments for goods or services. For example, the reporting requirements do not apply to birthday or holiday gifts, sharing the cost of a car ride or meal, or paying a family member or another for a household bill.

But the casual sale of goods and services, including selling used personal items such as clothing, furniture, and other household items for a loss on eBay and other online marketplaces, could generate a Form 1099-K for many people, even when they have no tax liability from those sales.

The complexity in distinguishing between these types of transactions factored into the IRS decision to delay the reporting requirements an additional year and to implement a $5,000 threshold for 2024.

The IRS is also looking to update Form 1040 and related schedules for 2024 to make the reporting process easier for taxpayers.

Will the $600 1099-K reporting threshold really come into effect for 2025? Only time will tell, but many believe $600 is too low, and legislation has been introduced to increase it to $10,000.

Lawmakers established the $600 threshold in 1954. If you adjust it for inflation, it would be $6,862 today.

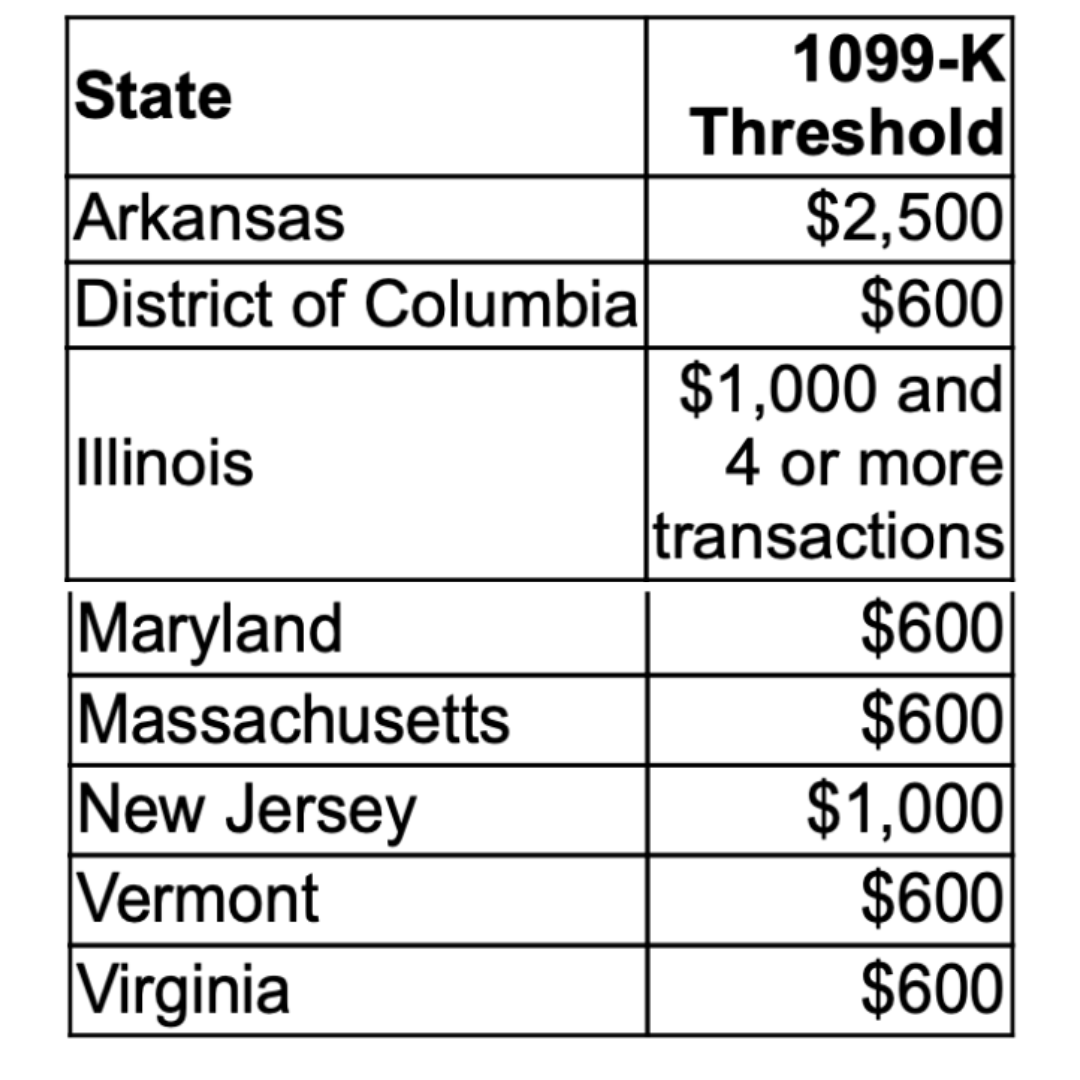

Seven States Have Their Own 1099-K Reporting Rules

Seven states and the District of Columbia have already abandoned the federal $20,000/200-transaction threshold for 1099-K filing and imposed lower thresholds. In these states, a 1099-K must be sent to the state tax agency and the payee if the lower state threshold is met.

Takeaways

The IRS postponed the implementation of the new 1099-K reporting rules for TPSOs such as PayPal, Venmo, and others, maintaining the current thresholds ($20,000 and 200 transactions) for the 2023 tax year.

Starting in 2024, these thresholds will be replaced with a $5,000 limit with no transaction count requirement, and for 2025 and beyond, a $600 threshold is planned with no transaction count.

The filing requirements for payments made by payment cards (credit, debit, gift cards) remain unchanged, with the 1099-K form being issued regardless of the dollar amount or number of transactions.

The IRS delayed the TPSO changes due to concerns over the potential influx of millions of new 1099-K forms, which could lead to confusion and errors among taxpayers and TPSOs. Additionally, differentiating personal payments from those for goods and services adds complexity, prompting the phased approach to lowering thresholds.

Seven states and the District of Columbia have diverged from federal thresholds, setting their own lower limits for 1099-K reporting.

There is ongoing debate over whether the $600 threshold set in 1954 and equivalent to $6,862 today, adjusted for inflation, is appropriate. Some federal lawmakers propose increasing it to $10,000, but that increase remains uncertain.

{kind=link}